.png)

Page 52:

Question 1: In situations with high risks, credit might create further problems for the borrower. Explain?

Answer:

- High-risk situations occur in rural areas because there the main demand for credit is for crop production which involves considerable costs on seeds, fertilisers, pesticides, water, electricity, repair of equipment.

- There is a minimum stretch of three of four months between the time when farmers buy these inputs and when they sell the crop.

- Farmers generally take crop loans at the beginning of the season and repay the loan after harvest.

- Repayment of the loan is crucially dependent on the income from farming.

- If a crop fails due to shortage of rain or for any other reason, a small farmer has to sell a part of the land to repay the loan.

- Failure of crops create further problems for the borrowers. Credit does not improve his earnings but leaves him worse off than before. Credit in high risks situations pushes the borrower into a debt trap, a situation from which recovery is very painful.

Question 2: How does money solve the problem of double coincidence of wants? Explain with example of your own.

Answer:

In a barter system where goods are directly exchanged without the use of money, double coincidence of wants is an essential feature. By serving as a medium of exchanges, money removes the need for double coincidence of wants and the difficulties associated with the barter system. For example, it is no longer necessary for the farmer to look for a book publisher who will buy his cereals at the same time sell him books. All he has to do is find a buyer for his cereals. If he has exchanged his cereals for money, he can purchase any goods or service which he needs. This is because money acts as a medium of exchange.

Question 3: How do banks mediate between those who have surplus money and those who need money?

Answer:

- People hold money as deposits with banks which pay an interest rate on them.

- People do not withdraw their cash daily.

- The banks, therefore, hold only 15 percent of their deposits as cash with themselves in order to pay the depositors who might come to withdraw money from the bank on any given day.

- Since, on any particular day, only some of its many depositors come to withdraw cash, the bank is able to manage with this cash.

- They use a major portion of the deposits to extend loans to those who need money.

- The banks make use of deposits to meet the loan requirements of the people.

- Thus, in this way, the banks mediate between those who have surplus money and those who need money. Banks charge a higher interest rate on loans than what they offer on deposits. The difference between the two is the main source of income of the banks.

Question 4: Look at a 10 rupee note. What is written on top? Can you explain this statement?

“Reserve Bank of India” and “Guaranteed by the Government” are written on top.

Answer:

In India, the Reserve Bank of India issues currency notes on behalf of the central government. The statement means that the currency is authorized or guaranteed by the Central Government. That is, Indian law legalizes the use of the rupee as a medium of payment that can not be refused in a setting transaction in India.

Question 5: Why do we need to expand formal sources of credit in India?

Answer:

We need to expand formal sources of credit in India due to the following reasons :

- The moneylenders or the agricultural traders charge a much higher interest on loans. They generally charge 5 percent per month whereas the banks charge about 10 to 15 percent per annum. The higher rate of interest does little to increase the income of the borrowers.

- The farmers who take loans from a trader are forced to sell their crops to him at a low price. As a result of it, the farmers suffer while the traders make a profit by selling grains at a higher prices.

- Higher interest means the borrower has to pay a major portion of his earnings to repay the interest and principal of the loan. This sometimes leads to debt trap for the borrowers.

- On the other hand, banks and cooperatives charge less interest and do not exploit the borrowers. Under these circumstances, there is need for expansion of formal sources of credit in India. It is also necessary that everyone receives these loans.

- This would also lead to higher incomes and many people could then borrow cheaply for a variety of needs. The formal credit should be distributed equally to benefit the poor from the cheaper loan.

- It may be added that cheap and affordable credit is crucial for the development of the country.

Question 6: What is the basic idea behind the SHGs for the poor? Explain in your own words.

Answer:

The basic behind the SHGs is to provide a financial resource for the poor through organizing the rural poor especially women, into small Self Help Groups. They also provide timely loans at a responsible interest rate without collateral. Thus, the main objectives of the SHGs are:

- To organize rural poor especially women into small Self Help Groups.

- To collect savings of their members.

- To provide loans without collateral.

- To provide timely loans for a variety of purposes.

- To provide loans at a responsible rate of interest and easy terms.

- Provide a platform to discuss and act on a variety of social issues such as education, health, nutrition, domestic violence, etc.

Question 7: What are the reasons why the banks might not be willing to lend to certain borrowers?

Answer:

The banks might not be willing to lend certain borrowers due to the following reasons:

- Banks require proper documents and collateral as security against loans. Some persons fail to meet these requirements.

- The borrowers who have not repaid previous loans, the banks might not be willing to lend them further.

- The banks might not be willing to lend those entrepreneurs who are going to invest in the business with high risks.

- One of the principal objectives of a bank is to earn more profits after meeting a number of expenses. For this purpose, it has to adopt a judicious loan and investment policies which ensure fair and stable return on the funds.

Question 8: In what ways does the Reserve Bank of India supervise the functioning of banks? Why is this necessary?

Answer:

The Reserve Bank of India monitors the amount of money that banks loan out, and also the amount of cash balance maintained by them. It also ensures that banks give out loans not just to profiteering businesses but also to small cultivators, small scale industries, and small borrowers. Periodically, banks are supposed to submit information to the RBI on the amounts lent, to whom, and at what rates of interest.

This monitoring is necessary to ensure that equality is preserved in the financial sector, and that small industry are also given an outlet to grow. This is also done to make sure that banks do not loan out more money than they are supposed to, as this can lead to situations like the Great Depression of the 1930s in the USA, which greatly affected the world economy as well.

Question 9: Analyse the role of credit for development.

Answer:

The role of credit for development is very significant as mentioned below:

- It helps in increasing economic activities of the borrowers.

- If credit is made available to the poor people on reasonable terms and conditions, they can improve their economic condition. This will help in the over all development.

- Credit may increase the activities in the secondary sector e., manufacturing sector. Thus, with credit people could grow crops, do business, set up small-scale industries. They could set up new industries or trade in goods. Therefore, credit is crucial for the country’s development.

Question 10: Manav needs a loan to set up a small business. On what basis will Manav decide whether to borrow from the bank or the moneylender? Discuss.

Answer: Manav will decide whether to borrow from the bank or the moneylender on the basis of the following terms of credit:

- rate of interest

- requirements availability of collateral and documentation required by the banker.

- mode of repayment.

Depending on these factors and of course, easier terms of repayment, Manav has to decide whether he has to borrow from the bank or the moneylender.

Question 11: In India, about 80 percent of farmers are small farmers, who need cultivation.

(a) Why might banks be unwilling to lend to small farmers?

(b) What are the other sources from which the small farmers can borrow?

(c) Explain with an example of how the terms of credit can be unfavorable for the small farmer.

(d) Suggest some ways by which small farmers can get cheap credit.

Answer:

(a) The banks might be unwilling to lend to small farmers because the farmers usually take crop loan at the beginning of the season and repay the loan after harvest. Repayment of loan is dependent on the income from farming. And in case of crop failure, repayment becomes impossible. In such cases, the recovery of loan from the small farmers becomes very difficult. The small farmers have to sell part of the land to repay the loan that is why banks do not want to give loans to small farmers.

(b) Small farmers usually borrow from moneylenders or agricultural traders.

(c) In case of failure of crops, it becomes impossible for small farmers to repay the loan by selling their crops. Thus in order to repay, the small farmers sell a part of the land. This leads to worsening of their condition. Sometimes, small farmers give collateral or security against loans. The collateral generally consists of land, building, vehicles, livestock. In case of nonpayment of loan, the lender may sell the collateral to recover loan. Under above conditions, the terms of credit become unfavourable for the small farmers.

(d) Besides banks, the other major source of cheap credit in rural areas are the cooperative societies or cooperatives. Members of a cooperative society, pool their resources for cooperation in certain areas. The cooperative accepts deposits from its members. With these deposits as collateral, the cooperative obtains loan from the bank. These funds are used to provide loans to members.

Question 12: Fill in the blanks:

- Majority of the credit needs of the __________households are met from informal sources.

- __________costs of borrowing increase the debt-burden.

- __________issues currency notes on behalf of the Central Government.

- Banks charge a higher interest rate on loans than what they offer on __________.

- _________is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender.

Answer:

- Majority of the credit needs of the poor households are met from informal sources.

- High costs of borrowing increase the debt-burden.

- Reserve Bank of India issues currency notes on behalf of the Central Government.

- Banks charge a higher interest rate on loans than what they offer on deposits.

- Collateral is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender.

Question 13: Choose the most appropriate answer.

(i) In an SHG most of the decisions regarding savings and loan activities are taken by

(a) Bank.

(b) Members.

(c) Non-government organization.

(ii) Formal sources of credit do not include

(a) Banks.

(b) Cooperatives.

(c) Employers.

Answer:

(i) (b)

(ii) (c)

Multiple Choice Questions

1. Which one of the following statements is most appropriate regarding a transaction made in money? [Delhi 2012]

(a) It is the easiest way

(b) It is the safest way

(c) It is the cheapest way

(d) It promotes trade

2. Which one of the following is the new way of providing loans to the rural poor? [Delhi 2012]

(a) Co-operative societies

(b) Traders

(c) Relatives and friends

(d) SHG’s

3. Which among the following authorities issues currency notes? [Delhi 2012]

(a) Government of India

(b) The State Bank of India

(c) Central Bank

(d) Reserve Bank of India

4. Banks provide a higher rate of interest on which one of the following accounts ? [AI 2012]

(a) Saving account

(b) Current account

(c) Fixed deposits for a long period

(d) Fixed deposits for a very short period

5. Which one of the following is the main source of credit for rich urban households in India ? [AI 2012]

(a) Formal sector

(b) Informal sector

(c) Moneylenders

(d) Traders

6. Which one of the following is an essential feature of the barter system?

(a) It promotes local market.

(b) It spreads social field of an individual.

(c) It requires double coincidence of wants.

(d) It is an easy way.

7. Which one of the following terms is not included against loans? [CBSE CCE 2012]

(a) Interest rate

(b) Collateral

(c) Documentation

(d) Lender’s land

8. What is main source of income for banks? [CBSE CCE 2012]

(a) Interest on loans

(b) Interest on deposits

(c) Difference between the interest charged on borrowers and depositors

(d) None of these

9. In which one of the following systems exchange of goods is done without use of money? [CBSE (CCE) 2012]

(a) Credit system

(b) Barter system

(c) Banking system

(d) Collateral system

10. Which of the following has an essential feature of double coincidence? [CBSE (CCE) 2012]

(a) Money system

(b) Barter system

(c) Financial system

(d) Banking system

11. What percent of their deposits do bank hold as cash? [CBSE(CCE)2012]

(a) 50 percent

(b) 80 percent

(c) 15 percent

(d) 60 percent

12. Which of the following is an asset that the borrower owns and uses as a guarantee until the loan is repaid to the lender? [CBSE(CCE)2012]

(a) Property

(b) Money

(c) Collateral

(d) Deposits

13. How many members a typical Self-Help Group Should have? [CBSE (CCE) 2012]

(a) 14 – 19

(b) 15 – 20

(c) 20 – 25

(d) 25 – 30

14. In a barter system: [CBSE (CCE) 2012]

(a) Goods are exchanged for money.

(b) Goods are exchanged for foreign currency.

(c) Goods are exchanged without the use of money.

(d) Goods are exchanged on credit.

15. About what percentage of their deposits is kept as cash by the banks in India? [CBSE (CCE) 2012]

(a) 25 %

(b) 20 %

(c) 15 %

(d) 10 %

16. Why do banks keep a small proportion of the deposits as cash with themselves? [Delhi 2011]

(a) To extend loan to the poor.

(b) To extend loan facility.

(c) To pay salary to their staff.

(d) To pay the depositors who might come to withdraw money.

17. The currency notes on behalf of the Central Government are issued by whom? [Delhi 2011]

(a) State Bank of India

(b) Reserve Bank of India

(c) Punjab National Bank

(d) Central Bank of India

18. Which one of the following is not a feature of money? [AI 2011]

(a) Medium of exchange

(b) Lack of divisibility

(c) A store of value

(d) A unit of account

19. Professor Muhammad Yunus is the founder of which one of the following banks? [AI 2011]

(a) Cooperative Bank

(b) Commercial Bank

(c) Grameen Bank

(d) Land Development Bank

20. Which one of the following is a modern form of currency? [Foreign 2011]

(a) Gold

(b) Silver

(c) Copper

(d) Paper notes

21. The Informal source of credit does not include which one of the following? [Foreign 2011]

(a) Traders

(b) Friends

(c) Cooperative Societies

(d) Moneylenders

Additional Questions

22. Anything which is generally accepted by the people in exchange of goods and services

(a) Money

(b) Barter

(c) Credit

(d) Loans

23. Both parties agree to sell and buy each other’s commodities

(a) Measure of value

(b) Store of value

(c) Double coincidence of wants

(d) Credit

24. Money acts as an intermediate in the exchange process. Which function of money is highlighted here?

(a) Measure of value

(b) Medium of Exchange

(c) Store of value

(d) All of them

25. Modern forms of money include

(i) Gold

(ii) Paper Notes

(iii) Coins

(iv) Silver

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (iii) and (iv)

(d) (ii) and (iii)

26. Mpney is accepted as a medium of exchange because the currency is authorised by

(a) Private sector

(b) Public sector

(c) Government

(d) People

27. Deposits in the bank accounts can be withdrawn on demand, therefore these deposits are called

(a) Returnable deposits

(b) Acceptable Deposits

(c) Demand deposits

(d) None of the above

28. It is a paper instructing the bank to pay a specific amount from the person’s account to the person in whose name it has been made is

(a) Paper note

(b) Cheque

(c) Chit fund

(d) Credit card

29. Banks use the major portion of the deposits to

(a) Keep as a reserve so that people may withdraw

(b) Meet their routine expenses

(c) Extend loans

(d) Meet renovation of the bank

30. An agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payment.

(a) Credit (loan)

(b) Chit fund

(c) Bank

(d) Cheque

31. Salim, the shoe manufacturer, to meet expenses obtains loans from two sources.

(i) Asks leather supplier to supply leather on credit

(ii) Bank

(iii) Obtains loan in cash as advance payment

(iv) Relatives

(a) (i) and (iii)

(b) (i) and (ii)

(c) (iii) and (iv)

(d) (ii) and (iii)

32. Swapna is unable to repay the moneylender and she is caught in debt. She has to sell a part of the land to pay off the debt. This situation is an example of

(a) Debt-loss

(b) Debt-Insecurity

(c) Debt-trap

(d) All of them

33. Whether credit would be useful or not, depends on

(i) Whether there is some support in case of loss

(ii) Action of competitors

(iii) Market response

(iv) Risks in the situation

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (ii) and (iii)

(d) (i) and (iv)

34. Terms of credit does not include

(a) Interest rate

(b) Collateral

(c) Cheque

(d) Mode of repayment

35. Krishak cooperative functioning in a village near Sonpur has ……………. farmers as members.

(a) 2500

(b) 2400

(c) 2350

(d) 2300

36. Formal sector loans include loans from

(i) Banks

(ii) Moneylenders

(iii) Cooperatives

(iv) Traders

(a) (i) and (iii)

(b) (ii) and (iv)

(c) (ii) and (iii)

(d) (i) and (iv)

37. Contribution of commercial banks as a source of credit for rural households in India in 2003 was

(a) 30 %

(b) 28 %

(c) 25 %

(d) 26 %

38. Organisation which supervises the credit activities of lenders in the informal sector.

(a) No organization

(b) Reserve Bank of India (RBI)

(c) State Government

(d) Central Government

39. Compared to the formal lenders, most of the informal lenders charge a much …………….. interest on loans

(a) Lower

(b) Constant

(c) Higher

(d) No interest

40. Formal sector meets only about …………… of the total credit needs of the rural people (in 2003)

(a) one third

(b) one fourth

(c) half

(d) whole

41. It is important that the formal credit is distributed more equally so that

(a) Poor can benefit from cheaper loans.

(b) Rich can get costly loans.

(c) Rich can get cheaper loans.

(d) None of the above.

42. After a year or two, if the SHG is regular in savings, it becomes eligible for availing loan from

(a) Cooperative societies

(b) Moneylenders

(c) Bank

(d) Traders

43. ……………. help borrowers overcome the problem

of lack of collateral and also they are the building blocks of organization of the rural poor.

(a) Government

(b) Banks

(c) Private sector

(d) SHGs

44. Almost all of the borrowers of Grameen Bank of Bangladesh are

(a) Men

(b) Women

(c) Senior citizens

(d) All of them

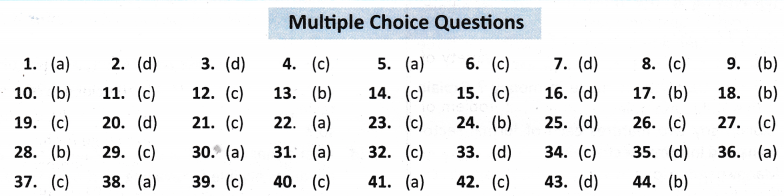

ANSWERS

- Chapter 1 The Rise of Nationalism in Europe

- Chapter 2 The Nationalist Movement in Indo-China

- Chapter 3 Nationalism in India

- Chapter 4 The Making of Global World

- Chapter 5 The Age of Industrialisation

- Chapter 6 Work, Life and Leisure

- Chapter 7 Print Culture and the Modern World

- Chapter 8 Novels, Society and History

NCERT Class 10 SST Solutions Geography:

- Chapter 1 Resource and Development

- Chapter 2 Forest and Wildlife Resources

- Chapter 3 Water Resources

- Chapter 4 Agriculture

- Chapter 5 Minerals and Energy Resources

- Chapter 6 Manufacturing Industries

- Chapter 7 Lifelines of National Economy

NCERT Solutions Class 10 SST

- Chapter 1 Power Sharing

- Chapter 2 Federalism

- Chapter 3 Democracy and Diversity

- Chapter 4 Gender Religion and Caste

- Chapter 5 Popular Struggles and Movements

NCERT Solutions for Class 10 Social Science

.png)